Pure life (payout on death) cover is usually not a problem with most insurers. You die, next of kin, business partner etc provide death certificate. Money is paid to beneficiaries with-in time frame.

However most policies are upsold to make brokerrs money, They include accidental death benefits, disability, partial credit repayment, lost of income etc. All these add to a tangled mess of wording. Then you add, payment returns, back to back cover.

They tell you that you save by taking out these combined/compound cover.

You need to look at the underwriter of the policy.

Stick to the big insurers, Sanlam, Old Mutual.

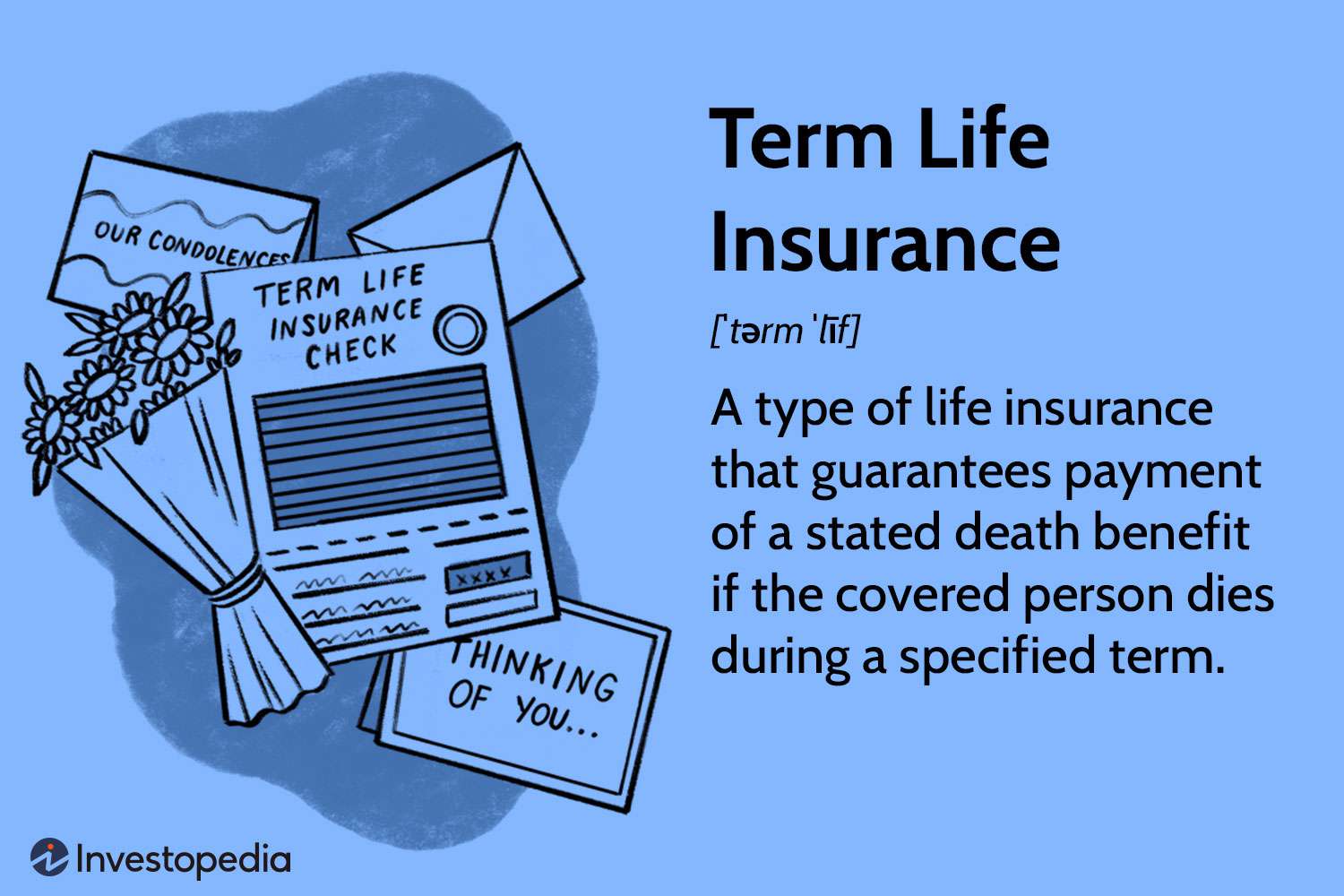

Term life insurance is a guaranteed life benefit paid to beneficiaries of the insured after death.

www.investopedia.com

There are certain insurers you should absolutely avoid

Neat info

This guide to ombudsman schemes in South Africa will help you find the right scheme to resolve your complaint against a company or organisation.

www.lawforall.co.za

Bad stuff

If you have a gripe with a long-term insurer, try to resolve it with the ombudsman's help.

mg.co.za

Santam

The Office of the Ombudsman for Long-term Insurance (OLTI) had its work cut out in the first half of 2021 with a record number of complaints.

www.fanews.co.za